How to Set Financial Goals as a California Teacher

We all know teachers should make more money -

but in the meantime, you need clarity and intention for your financial goals!

When I was teaching, I knew I didn't have a lot of money to mess around with and I also knew I wanted to be rich one day. In fact, I started listening to the Teach and Retire Rich podcast even during my teaching credential program. Eventually I knew I needed to come back to teaching later, and pivoted careers into financial planning. But before that, here are the financial goals that were on my mind!

Here are my top 8 ideas for you, a teacher, to consider taking on as a financial goal. I wrote these with California teachers in mind, but really, I think they could apply to any teachers across the US.

I STRONGLY recommend only picking 1 or 2 at a time, so you can make more progress and keep track of less stuff.

Mental load is real as I’m sure you know! And it's way more satisfying to see lots of progress on 1 or 2 goals, versus tiny progress on a bunch of goals.

1. Set a Budget For Classroom Stuff

If you're a seasoned teacher, I have a feeling you already do this...although my own mom has been teaching for over 20 years and I still do a little side eye at how much she spends on her own classroom.

As a new teacher, I know how tempting it was for me to go buy a bunch of stuff for my classroom - especially after following a ton of teacher influencer accounts on instagram and youtube! But I wish I had set a firm budget for myself and gotten clear on what was truly important and needed.

For example, I went and bought a ton of books for my classroom before the school year started, BUT we ended up getting a bunch of brand new books through the district AND of course, we had a library!

I also went and bought bookshelves and decor for my classroom, that the kids ended up damaging throughout the year.

Instead, what I am super glad I spent money on in my first few years teaching was a year-long curriculum from Teacher’s Pay Teachers when I had to switch from teaching English to Math. I share this to say that I DO think spending some money is a good idea, for your sanity!

If you’re not sure what amount to set as a budget, I would aim for either a set amount of money per month or try to stay under the annual educator expense deduction that you can get when you file your income taxes (which is currently $300 per year). I've witnessed many a teacher beg, borrow, and "steal" for funds to cover the rest and unfortunately, it's part of the deal in America right now for teachers.

2. Move Over On The Salary Schedule!

I’m lucky that my mom, an elementary school teacher, was constantly working on classes to help her move over on the salary schedule for her school district. She talked a lot about how much extra she would be making by moving over on the salary schedule, so I knew once I became a teacher, I should pay attention to that too!

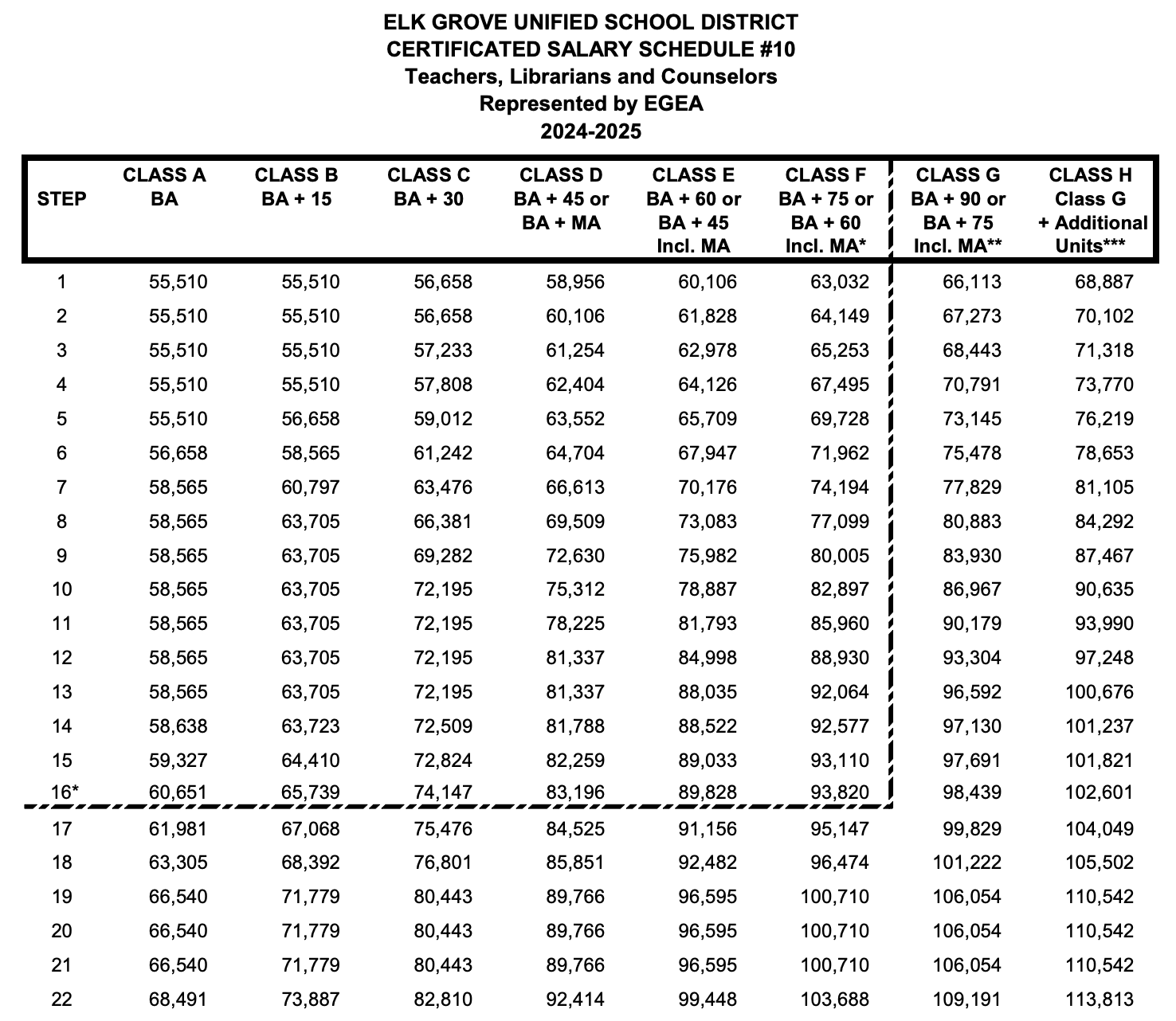

Let’s look at an example together to see how much money you might be leaving on the table over the course of your career:

See the EGUSD Salary Schedule above - if you're on Step 1, you're making $55,510 vs maxing out at $113,813 (very bottom right corner). Now obviously you won’t get there by your first year, so let’s compare year 22 without any extra classes vs maxed out - $68,491 vs $113,813

A $45,322 difference!

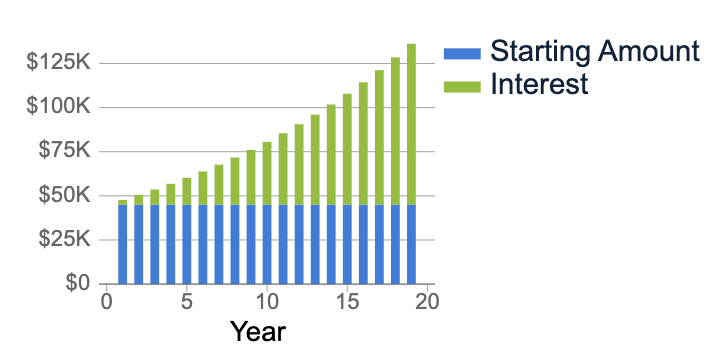

Let’s say just in year 22, the teacher who’s maxed out at $113k invests that $45k difference for their retirement. By age 65, that would be an extra $136k! See the graph below for a visual representation.

Now imagine that compounded year by year. 🤯

3. Get More Efficient at School To Increase Your Hourly Rate

This kind of blew my mind when I realized it.

By my second year of teaching, I realized that no matter how hard I worked (and how many hours I worked), I would never get paid more. There was just no way around it since we’re all on a salary schedule.

As a brand new teacher, you can imagine that I was working way more than my contracted hours to try to put together lesson plans and do my grading and so on. So I finally realized I needed to get more efficient to, basically, give myself an hourly raise.

For example, would you rather get paid $60,000 per year for 3000 hours of work or $60,000 per year for 2000 hours of work?

Obviously this is easier said than done, but I think it’s a worthwhile goal. Then your other hours can truly be for life, fun, and the stuff I cover in #8 at the end!

4. Figure Out Your Retirement Accounts

In case nobody told you, you can’t just live off of your pension.

It’s not designed that way.

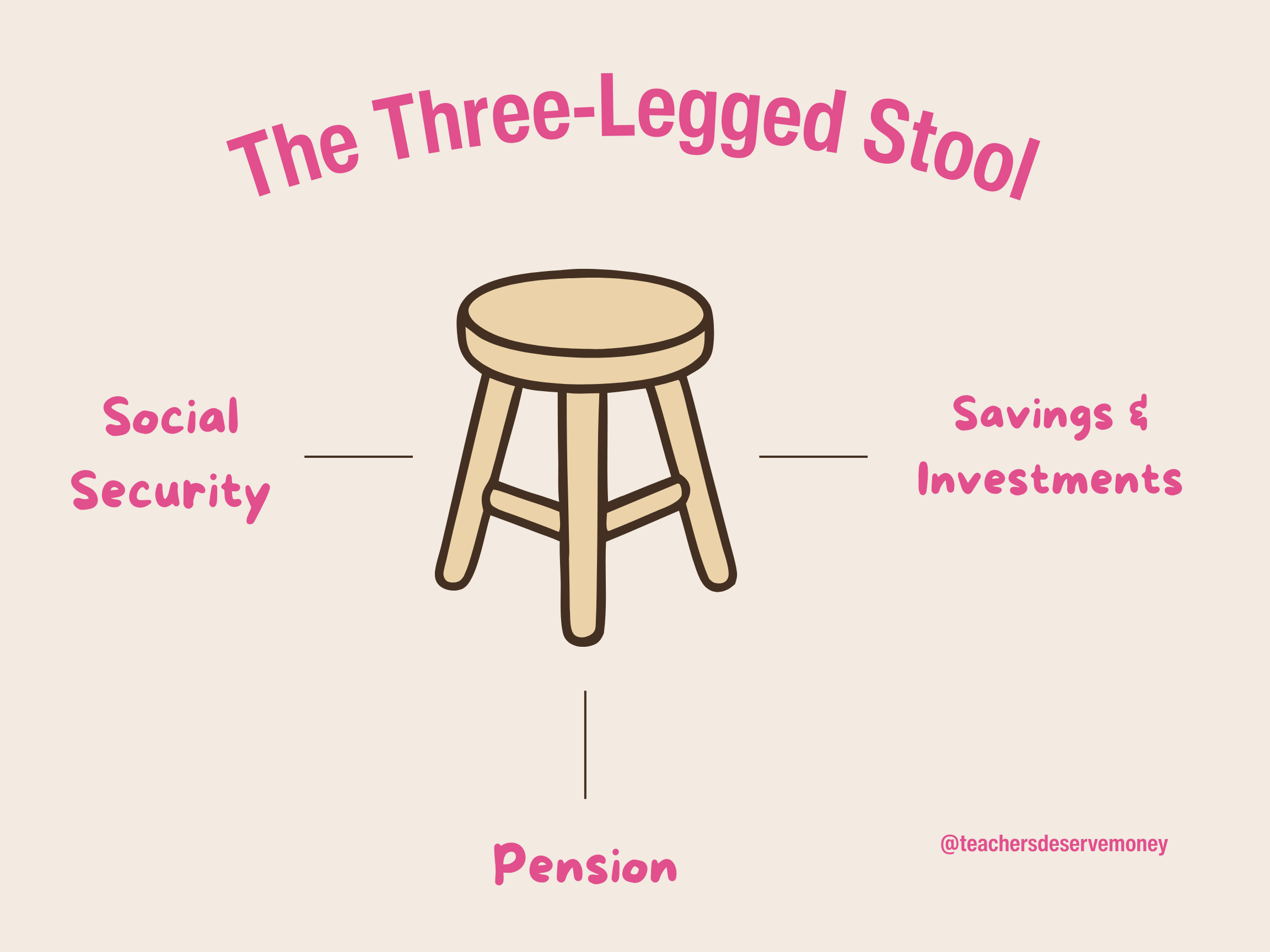

Here’s a good analogy - for most people, a solid retirement plan is made up of 3 different things like this stool above - a pension, personal savings and investments, and social security.

'Now, as a California teacher, you’re not paying into social security. So imagine you didn’t save or invest anything on your own and you only had the pension…then your stool wouldn’t be very sturdy, would it?

In California, your pension is through CalSTRS (California Teacher Retirement System). Your personal savings could be at any bank in your checking and savings accounts. Your personal investments could be through a retirement account at work through your school district, usually called a 403(b), and/or through a private retirement account like an IRA (that you can open at any place like Vanguard, Fidelity, Schwab, etc).

There's a TON more to go into here and figuring out the teacher retirement stuff can be a lot, so let me know if you’d like a separate blog/video series on it.

5. Apply for Teacher Grants

There are so many grants available to teachers - the hard part is finding the grants and applying!

I would start by checking out local businesses and seeing if they have any grants or donations available.

Another thing you can do is figure out what you want to teach and then search for grants related to it - for example, I searched eco grants for California teachers here and it led me to this! https://www.epa.gov/education/grants

If you know of any grants that teachers can apply to, please share and I'll start a separate blog post to keep track of them! My email is gabbi@teachersdeservemoney.com.

6. Budgeting

I know, I know. I think most teachers know they need to budget since they’re not making the big bucks.

But really! I come across teachers just budgeting on vibes!

You don’t have a lot to make financial mistakes with, so it’s worth testing out different budgeting methods to make the most of what you’ve got.

I applaud you for setting a budget for your classroom (well, hopefully you decided to do that from #1 above) - now it's time to make sure you're looking at your own personal finances too.

If a spreadsheet sounds like your worst nightmare, then grab a cute notebook and pen/pencil and just list out your biggest bills each month. That's usually rent/mortgage, student loans/other debt, then probably utilities and subscriptions. Give yourself permission to stop there if you've never budgeted before, and set a reminder to come back to this another day. Baby steps!

Once you've added up all your set bills each month, it's time to investigate your other spending. There are a lot of names for this, like "variable spending" or "flexible spending" - basically, all the other spending you're doing that fluctuates each time because you're making a decision on groceries, or dining out, or shopping.

While the gold standard would be to review a year's worth of past spending, start with just one week or one month at first.

When you add everything up, how much is it? Is that more or less than your paycheck for the month?

Give yourself time to just investigate before letting your feelings overwhelm you. Your first instinct might be to say "I shouldn't've spent money on XYZ!" but try to look at the numbers objectively first. As long as you're spending less than you make each month, you're doing AMAZING! And if not, try finding some easy wins - stuff you really don't care or want to spend money on that would be easy to stop.

Remember - small changes will yield small improvements! And if you're trying to make some big financial progress quickly, the same thing is true - you'll have to look at the biggest spending areas and make some drastic life changes to match your goal.

7. Organize Potlucks!

I know, we're reaching the end of the list and it might start to sound a bit more unhinged.

But even though I’m not teaching right now, I love doing this as often as possible to both save money and see friends!

This is especially fun when we come up with a fun theme, like Pi Day, or whenever I’m in the mood for a certain cuisine, like Korean food! Don’t forget to bring containers for leftovers!

There's a lot of benefits to organizing potlucks beyond helping your wallet. As we continue to live through our suspiciously-fascist-looking-times, it is really important to build community and solidarity with one another. Time spent eating together not only strengthens friendships, but it also gives you a sense of who you can rely on when times get tough(er).

8. Increase Your Income

Last but not least, be strategic about increasing your income beyond your teacher salary. You already probably know about signing up for extra duties at school or offering tutoring afterschool or during the summer.

- My mom is getting paid her normal rate by her district to tutor afterschool!

- I taught summer school to make extra money.

- Many of my teacher friends get paid to tutor their past students after school or during the summer.

- I know friends who dog walk or pet sit too!

- I had teachers who sold us snacks in our high school classrooms (not sure how 'allowed' this is).

- Whenever you create something new for teaching, throw it up on Teachers Pay Teachers! Even if it’s “ugly” - someone might still think it’s useful and worth paying for!

The options are endless, but I think the key here is to pick one thing (and don't spend too long agonizing over which thing to pick) and stick with it for a while. You are already a teacher - don't spread yourself even thinner with too many extra things!

Lastly, thank you.

As you know, I believe that teachers deserve money! Much more than they currently make in the US.

So thank you for all of your hard work and I hope this list provides some guidance in your financial life - you probably didn't get into teaching for the money, but taking care of your finances is a form of self-care.

Like I said earlier, don't try to tackle all of these at once! Pick one that resonates with you, whether it seems the easiest or sounds interesting, and focus on that for a year or so. If you need a little extra help, feel free to reach out via a virtual call, linked below, or contact me (at the bottom of the link here).